Sinking funds. Anything “sinking” sounds bad. In my opinion, this word isn’t the greatest for this important personal finance trick. Sinking funds are actually a vital part of a budget!

Let’s dive into more about what these funds are and how to incorporate them into your budget.

Disclaimer: I am not a financial planner or expert. All information in the post is based on my research, opinion and experiences. Any action you take based on the recommendations from this blog is at your discretion.

Affiliate Disclosure: This post contains an “affiliate link”. This means if you click on an affiliate link and purchase a product/ service, I may receive a small commission at no extra cost to you. However, I only recommend products I personally use, love, and/or believe will add value to my readers. For more information see my disclosures.

Importance of Sinking Funds

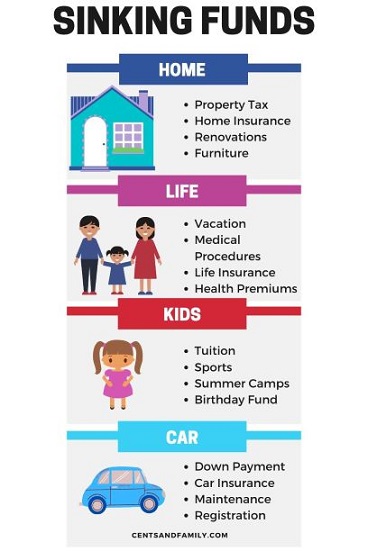

Putting money into a “sinking fund” is to save up money for a specific future expense. For example, you have expenses that you have to pay for annually such as home insurance, car insurance, sports registration for your kids, tuition etc. By understanding that you have to pay these expenses periodically, you make a plan to stash money away on a regular basis for these expenses. Other bigger expenses that you can save up money for include a down payment for a car or home or for a major home renovation.

Instead of scrambling to pay for these expected expenses, you have money ready to pay for them when the time comes. It will help you avoid going into debt and to be more organized with your personal finances.

Sinking funds vs Emergency Fund

So how are sinking funds different from emergency funds? Saving up for a sinking fund is saving up for a known expense. An emergency fund is reserved for those unexpected “emergency” expenses such as if you require to buy a new fridge to replace your broken one or if you have lost your job. Both are an important part of a budget and I recommend that you have both.

How to Use Sinking Funds in a Budget

Most budgets reflect what is coming in and out on a monthly interval. So what happens if you have an expense (i.e. property taxes) that you pay annually? How would we put that annual expense into a monthly budget?

Answer: Take the amount of the annual expense and divide it by 12. The monthly amount is what you should record in your monthly budget.

How to keep track of your sinking funds

Keeping track of the amount you saved up for each sinking fund is important too. The best way to do this is to “give every dollar a job” in your savings account. This method will allow you to easily keep track of what each dollar is for in your savings. I highly recommend creating your own spreadsheet to keep track. If you are not familiar with how to use a spreadsheet, take a look at this post: How to Use 4 Spreadsheet Functions to Create a Budget

A personal budget should have sinking funds incorporated into it. Sinking funds are the best way to save up for a known future expense. This practice will help people stay out of debt. Get in control of your finances to have the life you deserve.

Let’s start sinking those funds!

Minda’s Reading Recommendations on Personal Finance:

You may also like:

Sinking funds are so important for my budget! They make everything so much easier and my budget much more organized!